Hold the Line: A Veteran's Field Guide to Defeating Predatory Lenders

Predatory lenders do not care about your mission, your service, or the pressure on your household. They care about one thing: whether they can get in front of a veteran who needs cash fast and convert stress into a long stream of payments.

Veterans are a prime target because many households have one thing lenders love: predictable income. A VA deposit is steady. That stability should be a strength. In the wrong hands, it becomes a collection strategy pointed directly at your future.

This is not a lecture about never borrowing. It is a field guide for recognizing the ambush before you step into it.

Why Predators Focus on Veterans

Predatory lending is built on urgency. The product is designed to look like relief in the moment and extraction over time. Payday loans, title loans, junk installment loans, and cash-advance apps all use the same playbook: simplify the approval, shrink the payment, and bury the real cost.

That model works best when the borrower feels boxed in. A veteran dealing with a car repair, a rent gap, or a utility shutoff notice is exactly the situation they want. Add a predictable VA payment to the equation, and the lender sees a payment stream they can position themselves in front of month after month.

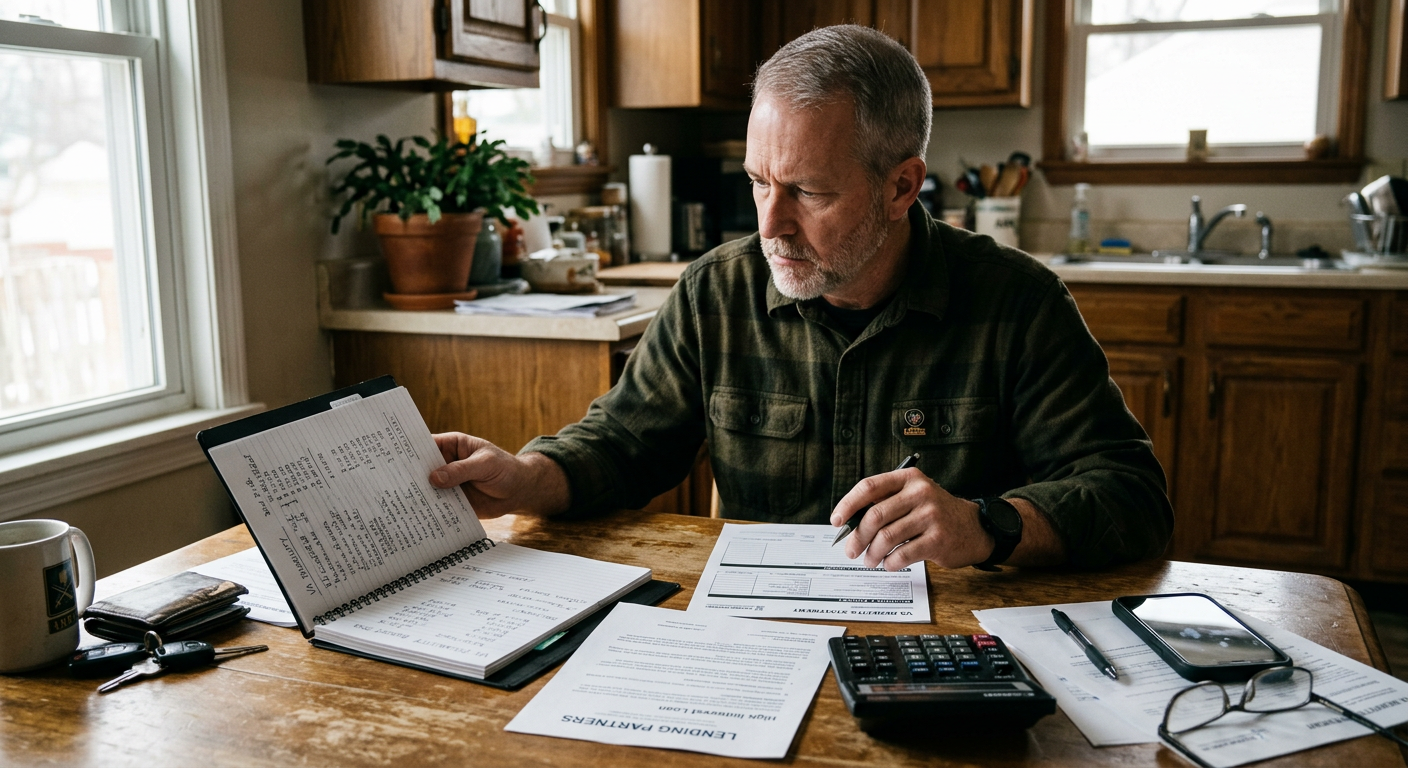

The Five-Point Contact Drill Before You Sign Anything

Before you accept any emergency loan, stop and run this drill in order. If you cannot answer these clearly, you are not ready to sign.

- Identify the real APR: not the "fee," not the biweekly payment, not the teaser number. The APR tells you what the money actually costs.

- Calculate total payoff: ask, in dollars, how much will leave your pocket from first payment to final payment.

- Check the rollover trap: if the lender benefits when you extend, refinance, or miss once, the deal is designed to expand under stress.

- Measure the hit to next month: if the payment turns next month's budget into a crisis, you did not solve an emergency. You moved it.

- Force a delay: take 24 hours before signing unless utilities are being shut off that same day. Time is the enemy of bad lenders.

This is where discipline matters more than emotion. Predators win when the decision is made in ten minutes, on a phone, with no worksheet, no calculator, and no pause.

Red Flags That Should End the Conversation Immediately

- "No credit check" as the main selling point: that usually means the lender expects to profit from bad terms, not good underwriting.

- Pressure to sign today: if the offer gets worse the moment you ask for time, it was never built for your benefit.

- Vague answers about fees: legitimate lenders can explain every dollar in plain English.

- Collateral tied to your vehicle or bank access: title loans and aggressive ACH authorizations are how small shortfalls turn into major losses.

- Marketing built around military identity: flags, uniforms, and patriotic language do not make bad math less dangerous.

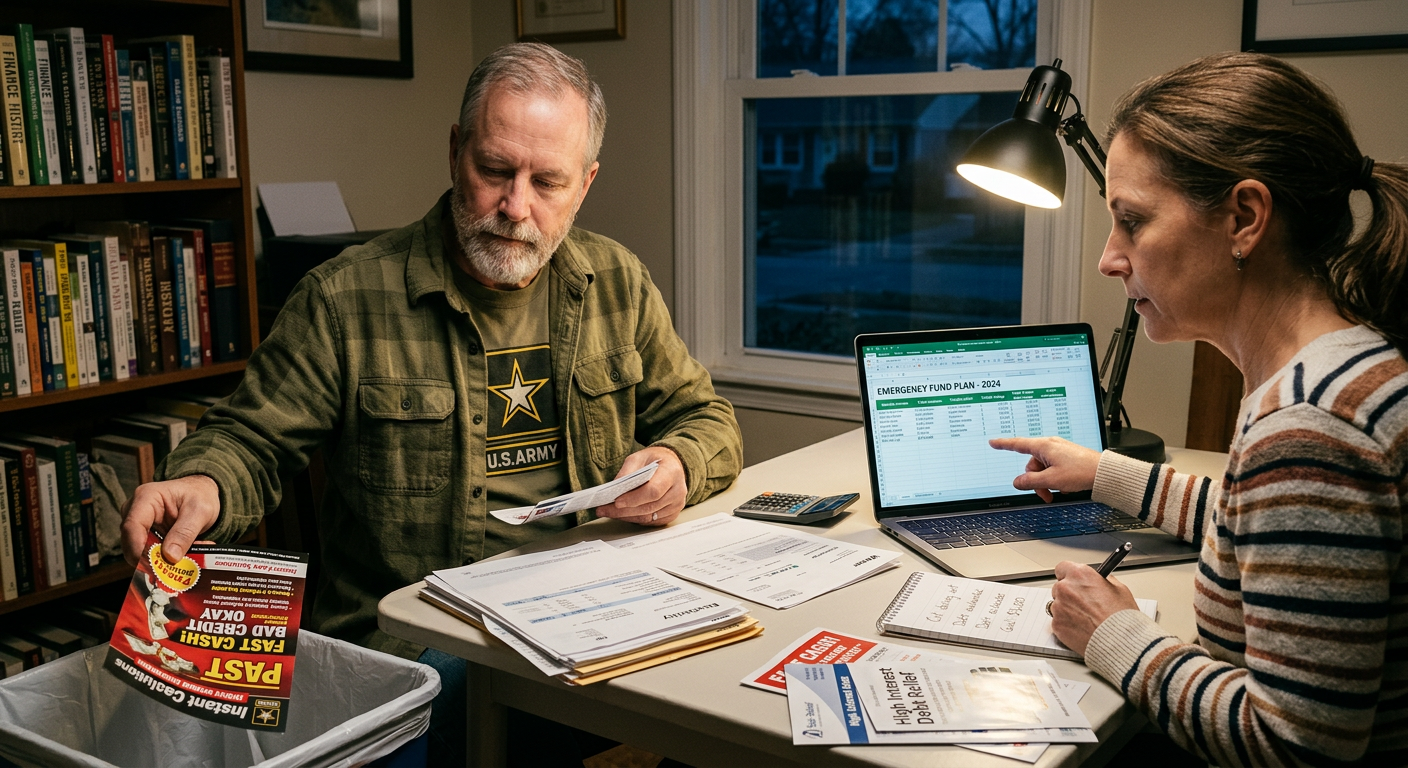

Better Options When the Situation Is Real

If the emergency is legitimate, the answer is not to pretend you can wish it away. The answer is to choose the least damaging source of relief available.

- Start with your bank or credit union: many offer small emergency loans or hardship options at rates that are still expensive, but survivable.

- Call the biller before you borrow: utilities, hospitals, landlords, and insurers often have payment plans that cost far less than a rushed loan.

- Use veteran relief channels: county VSOs, local veteran service organizations, relief societies, and community charities can sometimes close a short-term gap without trapping you in interest.

- Sell time, not your future: if you have assets you can liquidate safely or a discretionary expense you can suspend, do that before borrowing against next month.

How to Make Yourself Harder to Exploit

The long-term defense is operational, not motivational. You do not beat predatory lenders with better intentions. You beat them by reducing how often you need a fast decision under pressure.

- Build a $500 emergency buffer first: this is the first layer of armor between you and panic borrowing.

- Separate bill money on deposit day: when your VA payment lands, move essentials immediately so the operating balance is honest.

- Keep a written emergency action list: note who you call, what you cut, and what you can sell before debt enters the picture.

- Run a weekly financial check: 15 minutes of review can prevent a rushed decision that costs you six months.

Final SITREP

Predatory lenders are not offering rescue. They are monetizing your urgency. Veterans need to treat that for what it is: a threat to readiness, stability, and long-term control.

Slow the decision down. Check the math. Use the least damaging option first. Then build the buffer that keeps you out of the kill zone next time.

If you want one place to run that battle rhythm, use BattleStation. It is built to help veterans protect cash flow, see risk early, and make calm decisions before bad lenders get a vote.

Share this article

Help others discover this content

Related Articles

The New Military Financial Literacy Act: What Veterans Need to Know in 2026

A bipartisan bill just passed that could change how veterans learn about money. Most have not heard of it yet. Here is what it actually does, why it matters, and what you can do right now.

How Veterans Can Build an Emergency Fund With VA Benefits Without Killing Cash Flow

Living on VA disability, GI Bill stipends, or mixed benefit income does not mean you cannot save. Here is a practical ladder from your first $500 to three months of expenses, built around the money you actually receive.

How Veterans Can Read the 2027 VA Budget Without Building Their Financial Plan on Hype

The FY2027 VA budget proposal hit $488.2 billion and the headlines went wild. But a budget request is not a deposit in your account. Here is how to use benefits updates responsibly in your personal financial plan instead of budgeting off hype.