How Veterans Can Read the 2027 VA Budget Without Building Their Financial Plan on Hype

Every time the VA budget makes the news, I watch the same thing happen. A headline says "record $488 billion for veterans" and within hours, people are adjusting their spending expectations based on a number that has not been signed into law. Social media fills up with speculation about new benefits, higher rates, expanded programs. Then months pass, Congress does whatever Congress does, and the actual outcome looks different from the headline.

I am not saying ignore the budget. I am saying read it like an adult, not like a press release. There is real information in the FY2027 VA budget proposal that matters for your planning. But the line between "useful data point" and "financial fantasy" is thinner than people realize.

Here is how to pull what actually matters out of the numbers and keep your household budget grounded in reality.

A big VA budget headline is not the same as a personal raise

The FY2027 VA budget request totals $488.2 billion. That is a 7.7% increase over the FY2026 enacted budget. Those are real numbers from the VA's own budget page, updated April 7, 2026.

Sounds great. But what does it mean for your bank account? Probably nothing yet.

A budget request is a proposal. It is the executive branch saying "here is what we want Congress to fund." Congress then takes that proposal, argues about it, modifies it, sometimes guts parts of it, and eventually (if they get around to it) passes an appropriations bill. Sometimes they do not pass one at all and the government runs on continuing resolutions that freeze spending at prior-year levels.

The Military Times described it plainly: the proposal is a blueprint for Congress to consider, not a final enacted law. Stars and Stripes called it a blueprint and a starting point. Those are accurate descriptions. A blueprint is not a building.

So when you see "$488 billion for veterans" in a headline, what you are actually seeing is a request. The final number could be higher, lower, or stuck in legislative limbo for months. Building your budget around a request is like counting a job offer you have not received.

What the FY2027 VA budget actually proposes

Now that we have the context right, let me walk through what the proposal actually says, because there is useful information here even if none of it is final.

The $488.2 billion breaks into two big categories:

- $131.9 billion in discretionary funding (things Congress votes on each year, like VA medical system operations)

- $337.6 billion in mandatory funding (programs required by law, like disability compensation and pensions)

That mandatory number is up $22.6 billion, or 7.2%, above 2026. It covers compensation and pensions, readjustment benefits, housing and insurance, and the Toxic Exposures Fund. These are the line items that directly affect most veterans' monthly checks.

On the health care side, the request includes $96.2 billion for care provided in the VA medical system and $42 billion for community care. The budget would support 9.2 million veterans enrolled in VA health care and provide disability compensation to more than 7.4 million veterans.

Those numbers tell you where the administration wants to put money. They do not tell you where money will actually go. Important difference.

What is confirmed versus what is still a proposal

This is where a lot of veterans get tripped up. Some of the numbers in the budget discussion reflect things that have already happened. Others are forward-looking proposals that require Congressional action.

Already happened and confirmed:

- The VA processed 3,001,734 disability compensation and pension claims in 2025, above the prior record of about 2.49 million in 2024.

- The VA distributed $195 billion in compensation and pension payments to more than 6.9 million veterans and survivors in 2025.

- The claims backlog fell 63% since January 20, 2025, dropping from 264,717.

Those are backward-looking facts. They already happened. You can use them to understand the trajectory of VA operations. The faster processing and reduced backlog are real, and if you have a pending claim, that trend line matters to you.

Still proposals and not yet enacted:

- The specific $488.2 billion total for FY2027

- The $337.6 billion mandatory spending figure

- The $96.2 billion for VA medical system care

- The $42 billion for community care

Do not plan your 2027 finances around these numbers. They might land close to these figures. They might not. Until Congress acts, they are projections.

How to use benefits updates in a personal budget without getting burned

Here is what I tell veterans who want to use budget news in their financial planning without making bad assumptions.

First, your budget should be built on confirmed deposits. Your disability compensation rate is set by law and adjusted annually through COLA. Your current monthly amount is a fact. A proposed budget increase is not a fact. Plan off the number that hits your bank account today.

Second, treat proposed changes as a planning horizon, not a guarantee. If the budget proposal signals that the VA is expanding community care funding, that is useful to know. Maybe it means shorter wait times at community providers in 2027. Maybe it means broader eligibility for certain referrals. But you should not change your health care strategy until you see those changes actually implemented.

Third, keep a watch list. Write down the specific proposals that would affect you personally. Track them through the legislative process. If you have pending claims and the claims backlog is dropping, that is a positive signal for your timeline. If Congress is debating changes to the Toxic Exposures Fund, and you have a PACT Act claim, follow that thread. But following is not the same as assuming.

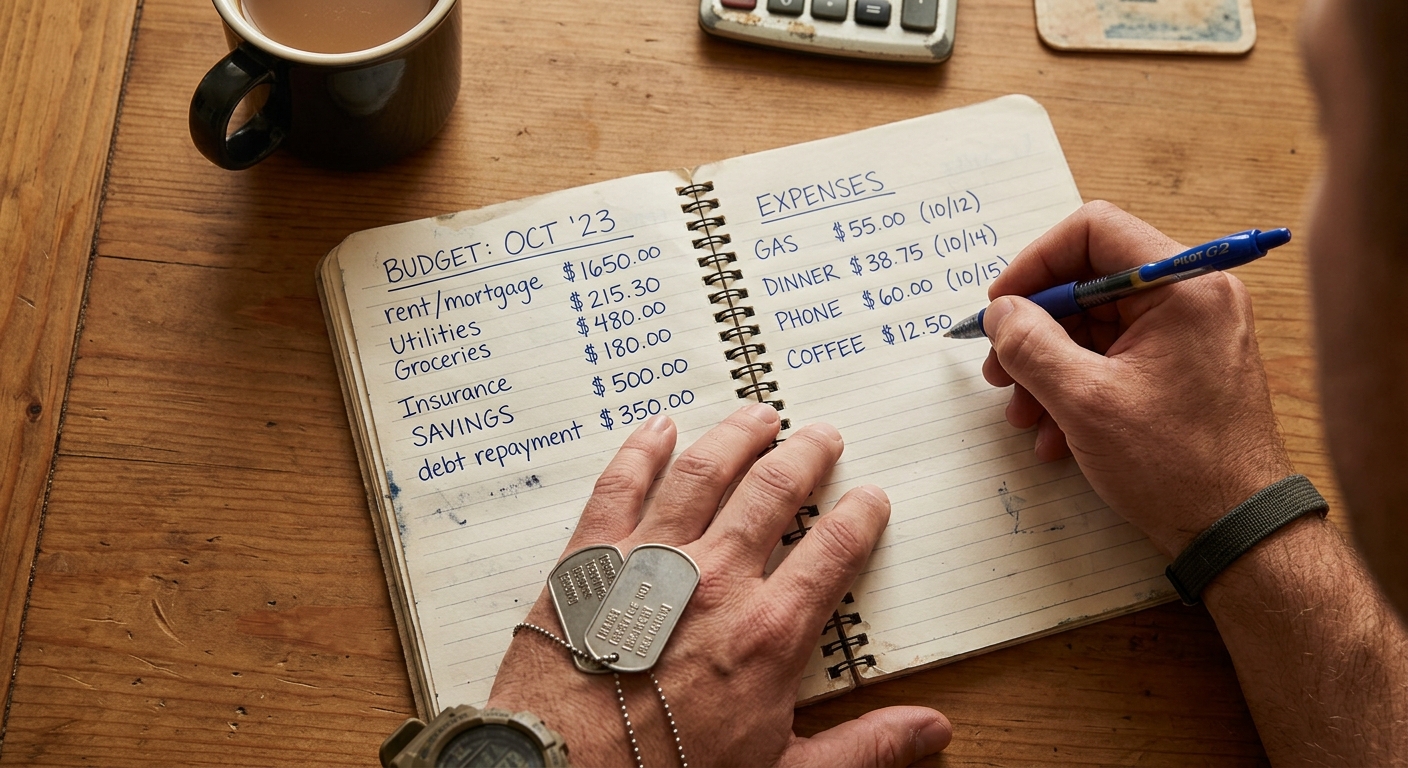

The 3-bucket system: bills, buffer, and future transition goals

I have seen too many veterans run their finances month-to-month with no structure. Here is a simple framework that works whether the budget passes as proposed or gets reworked entirely.

Bucket 1: Bills. This is your non-negotiable monthly spend. Rent or mortgage, utilities, food, insurance, transportation, phone. Add it up. Your confirmed monthly income (disability compensation, employment income, any other locked-in sources) needs to cover this bucket completely. If it does not, that is problem number one and no VA budget proposal fixes it.

Bucket 2: Buffer. This is your emergency fund and short-term cushion. Target at least one month of expenses to start, then build toward three. The buffer exists so that when something unexpected hits, a car repair, a medical copay, a delayed payment, you do not end up in a payday loan cycle. I have written about predatory lending targeting veterans before. A buffer is your first line of defense against those traps.

Bucket 3: Future transition goals. This is where proposed budget changes might eventually matter. If the VA expands VR&E funding, or if new education benefits come through, those could open doors for career transitions, certifications, or training. But you plan this bucket with money you can afford to wait on. Do not quit your job because a budget proposal suggests expanded retraining benefits. Wait until the ink is dry and the benefit is in your hand.

The 3-bucket approach works because it separates what is real from what is possible. Bills are real. Buffer is real. Transition goals can incorporate proposals, but only as potential upside, never as a baseline assumption.

Mistakes veterans make when budgeting off headlines

I keep seeing the same errors. Maybe you recognize some of these.

Counting a proposed benefit increase before it passes. A veteran sees that mandatory spending is proposed to increase by $22.6 billion and assumes their monthly check is going up. Mandatory spending increases do not automatically mean individual payment increases. They can reflect more veterans receiving existing benefits, PACT Act claims being processed, or actuarial adjustments. Your individual rate is tied to your rating percentage and the annual COLA, not to the total mandatory spending line.

Confusing budget categories with personal benefits. The $96.2 billion proposed for VA medical system care does not mean you individually will receive more or better care. It might mean the VA can hire more staff or reduce wait times. Or it might get cut in committee. The point is that aggregate numbers do not translate directly to individual outcomes.

Making large financial commitments based on expected changes. Signing a lease on a more expensive apartment because you expect a benefit increase. Financing a vehicle because you assume expanded education benefits will free up cash. Taking on debt because "the budget looks good for veterans." These are real decisions I have heard about from real people. If the proposal changes or gets delayed, the debt does not.

Ignoring what is already confirmed in favor of what is speculative. The VA processed over 3 million claims last year. The backlog dropped 63%. If you have a pending claim, that confirmed trend is more relevant to your near-term finances than any proposed budget figure. Focus on what is already in motion.

What you should actually do this week

Pull up your bank account. Look at what the VA deposited last month. That is your number. Not the number in the headline, not the number in the proposal, not the number someone posted on Reddit. Your deposit.

Now build your 3-bucket plan around that number plus any other confirmed income. If you have a pending claim, do not budget for it until it is decided. If you are waiting on a COLA adjustment, use last year's rate until the new one hits your account.

Keep an eye on the FY2027 budget as it moves through Congress. Follow it. Understand it. But do not spend it before it arrives.

That is the difference between being informed and being reckless. Read the budget. Understand the proposals. Then plan off what is real.

Download the veteran benefits budget planner

I put together a budget planner built around the 3-bucket system. It separates your confirmed income from proposed or pending benefits, tracks your bills and buffer, and gives you a clean view of where you actually stand. No hype, no guesswork, just the numbers that matter.

Download the veteran benefits budget planner here and stop building your financial plan on headlines.

Sources: U.S. Department of Veterans Affairs budget page (updated April 7, 2026), Military Times (April 7, 2026), Stars and Stripes (April 6, 2026), Newsweek (April 2026).

Share this article

Help others discover this content

Related Articles

How Veterans Can Use VR&E and VA Disability Together Without Blowing Their Budget

VR&E can cover tuition, books, and supplies while your disability check keeps the lights on. But the subsistence math is tricky, and picking the wrong payment path can leave you short. Here is what to watch for.

How Veterans Can Avoid Predatory Loans and Build a Cash Buffer on VA Benefits

A practical guide for veterans on fixed income to spot predatory lending traps, use the VA Veterans Benefits Banking Program, and build a real cash buffer without sacrificing rent, food, or meds.

How Veterans Can Use VR&E, the GI Bill, and VET TEC 2.0 to Transition Into Tech Without Blowing Up Their Budget

A no-fluff breakdown of how to stack VR&E, the Post-9/11 GI Bill, and VET TEC 2.0 for a tech career pivot — without draining your savings or burning entitlement you might need later.