Why Veterans Are Uniquely Built for Tech Careers (And the Financial Moves to Make Before You Transition)

Jasmine Paul was an Air Force finance officer when she noticed something strange. Her airmen were maxing out credit cards. Some of them were sleeping on friends' couches. Despite holding steady military paychecks, they had no idea how to manage money. Paul started teaching them herself. Over the next few years, she helped 110 service members pay off more than $350,000 in debt. She did this as a side activity, while doing her actual job.

That story is not unique. It is a pattern. Veterans know how to execute under pressure, manage logistics at scale, and lead people through ambiguous situations. Tech companies have figured this out. The GI Bill has been used to fund coding bootcamps and CS degrees. Veterans are showing up in cybersecurity, data analytics, project management, and software engineering in growing numbers.

But here is the part nobody talks about enough: the financial transition is where people get wrecked. Not the career change. The money.

What You Actually Bring to Tech

Let me be direct about something. The veteran-to-tech pipeline works because of the actual skills you developed in service, not because companies feel good about hiring veterans. Here is the real breakdown.

Operational thinking. In the military, you learned to take ambiguous situations with incomplete information and make decisions that had real consequences. That is not a soft skill. That is exactly what product managers, operations leads, and founders do every day. Most civilian candidates for these roles have never been tested that way.

Leadership under stress. You have been the person responsible when things went wrong. You know how to stay functional when the situation is bad. That is a rare quality in tech, where deadlines, scaling issues, and pivots create constant low-level stress. The veterans who thrive in tech are the ones who stop apologizing for their military background and start articulating what they actually learned from it.

Mission orientation. Tech employees who actually care about what they are building are rare. Veterans who want a mission, who want to feel like the work matters, translate directly into people who show up with motivation when things get boring or hard.

The resume gap is real, though. Civilian hiring managers do not always know how to read military experience. Your job is not to make them feel comfortable with your background. It is to translate it into the language they understand, as specifically as possible, on paper and in interviews.

The Financial Traps That Derail Transitions

Here is where I have seen the most veteran transitions fall apart. It is not the job search. It is not the skills gap. It is the period between your last military paycheck and your first civilian one, and the decisions you make during that window.

Severance Evaporation

If you are separating rather than retiring, you may receive severance pay. Here is what most people do not know: the VA counts severance pay as income, and it can affect your disability compensation for months afterward. The rules are specific and depend on whether you are receiving TDIU, the nature of your severance, and how it is structured. Before you spend that money, talk to a VSO or a veterans disability advocate about how it interacts with your benefits. This is not a small thing. I have seen veterans lose thousands in VA benefits because they did not plan for this window correctly.

Healthcare Gaps

TRICARE ends on a specific date. If you are not starting your civilian job immediately, you need to understand exactly when your coverage stops and what your options are. COBRA can be expensive. VA health care enrollment is an option but it is not instant, and not all veterans qualify for comprehensive VA health benefits. The community care network exists as a backup, but you have to be enrolled to access it. If you have any ongoing medical needs, do not let this slip.

Relocation Costs

Tech jobs are concentrated in specific cities. If you are moving from a military installation to a tech hub, you are probably underestimating what that costs. Housing deposits, moving trucks, first month rent, the gap between your old cost of living and your new one. If you are coming from a low-cost-of-living area to somewhere like San Francisco, Austin, or Seattle, the math hits hard. Most veterans budget for the move itself and forget about the three months of higher living expenses before they normalize.

The Pay Structure Trap

Military pay is predictable. You know exactly what you get paid on the first and the fifteenth. Civilian tech pay is often structured differently: base salary plus equity, performance bonuses, signing bonuses that vest on specific schedules. A $130,000 offer sounds better than it is if $40,000 of it is in stock that vests over four years and you need to move to a high-cost city immediately. Read your offers carefully. Ask specifically about the cash component, the equity structure, and when benefits start.

Banking That Actually Works for Transitioning Veterans

Jill Castilla is a veteran, a military spouse, a Blue Star mom, and the CEO of ROGER Bank. She saw young service members at basic training filling out direct deposit forms incorrectly and waiting weeks for their first paycheck because of paperwork errors. That observation led her to build a bank specifically for the military community.

ROGER Bank is FDIC-insured through Citizens Bank of Edmond, a 125-year-old community bank, combined with a modern fintech platform. The fee-free structure is not a marketing pitch. There are no monthly maintenance fees, no minimum balance requirements, and the direct deposit process is designed to get new service members paid correctly from day one.

For veterans in transition, the banking details matter more than people think. When you are moving between jobs, between locations, between financial systems, having a bank that understands military pay structures, PCS moves, BAH, and combat pay means you can actually talk to someone who gets it when something goes wrong. ROGER Bank's customer support is staffed by veterans. That is not a gimmick. That means when you call with a problem, the person on the other end knows what a LES is and why your separation paycheck timing is going to be weird.

The current rates as of early 2026: 2.00% APY on checking, 3.61% APY on savings. Most traditional banks are offering close to nothing on checking accounts. If you are building an emergency fund during your transition period, every percentage point matters, and fee-free banking means more of your money actually stays yours.

You can open an account before you ship out of your current location. No minimum deposit. No cosigner required if you are starting from zero. The app lets you lock your card, set alerts, and track spending. For veterans navigating a transition with a lot of moving parts, that simplicity is worth something.

The Compound Advantage: Why Your 20s and 30s Matter More Than You Think

Air Force veteran Jasmine Paul put it simply: "There is life after the military, and you are going to be OK." That is not just motivational language. It is financially true, and here is the math behind it.

If you start investing $300 a month at age 25, earning an average 7% annual return, you will have approximately $567,000 by age 65. If you start at age 35, you will have approximately $268,000. The ten-year difference in starting age costs you more than $299,000. That is not a typo.

Compound interest is not a new idea. But the application for veterans transitioning into tech careers is specific. You are probably entering a field where your earning potential is higher than it was in the military. You have access to retirement accounts that civilian employers offer: 401(k) with employer match, Roth IRAs, HSAs. The window to start is now, not after you "get settled."

DAV, the organization of disabled American veterans with more than one million members and 1,200 local chapters, runs DAV Patriot Boot Camp specifically to help veterans navigate the transition to civilian and entrepreneurial life. The program is free. The mentoring is free. For veterans who are thinking about starting businesses or navigating civilian career transitions, it is one of the most practical resources available. If you are in that window between separation and your first civilian role, look at what they offer.

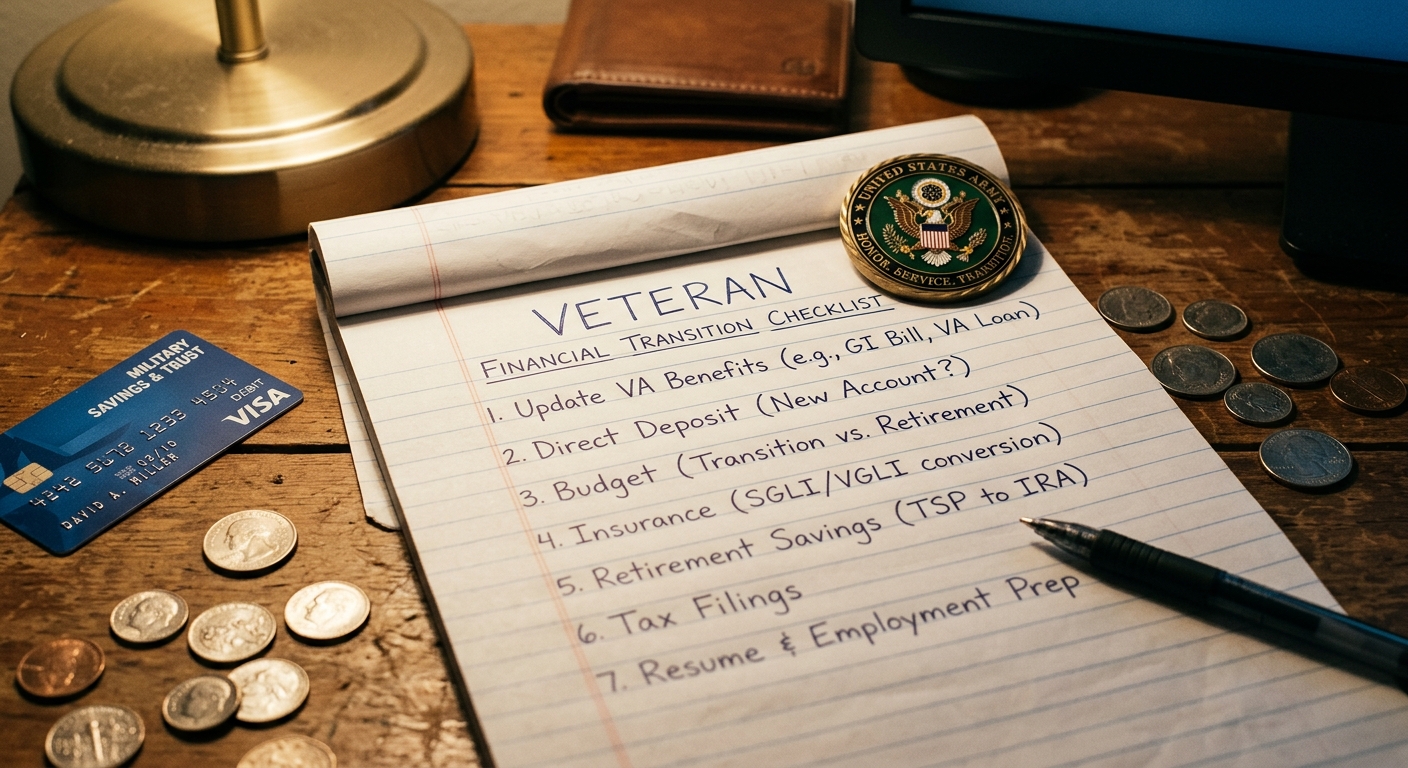

The Checklist

Before you separate, before you take that civilian offer, before you pack the U-Haul:

- Get your VSO involved in your severance planning. Do not spend it without understanding how it interacts with your VA benefits.

- Know exactly when TRICARE ends and what your healthcare bridge looks like.

- Open a fee-free bank account that understands military pay. ROGER Bank exists for exactly this.

- Start a retirement account before your last military paycheck, even if it is small. The compound window is real.

- Get clear on the cash versus equity breakdown in your civilian offer before you sign anything.

- Budget for three months of higher cost of living at your new location, not just the move itself.

- Connect with DAV Patriot Boot Camp if you are navigating the transition. Free resources, free community, free mentoring.

The career transition is the part everyone talks about. The financial transition is where people actually stumble. You have already proven you can handle hard things. This is just another hard thing with a specific checklist.

Share this article

Help others discover this content

Related Articles

Top Chronic Pain Symptoms Veterans Ignore (and Why Documentation Matters)

Veterans are trained to push through pain. That discipline is an asset in combat and a liability when you are building a disability claim. Here are the symptoms you are probably dismissing, and what happens to your case when you do.

World Mental Health Day, Every Day: A Year-Round Support Plan for Veterans

One awareness day a year is not a mental health strategy. If you are a veteran who wants actual, sustained support, here is what a real year-round plan looks like — with specific resources, what they cost (free), and how to stay consistent when motivation disappears.

Does the VA Still Accept DBQs in 2026? What Changed and What Did Not

The VA keeps moving the goalposts on Disability Benefits Questionnaires. Some are still accepted, some are not, and the rules changed again in 2025. Here is what you need to know before your next claim.