How Veterans Can Spot Claims Predators Before They Touch a Dollar of Your VA Benefits

I want to be blunt up front. The single fastest way to lose money during a VA claim is not the rating decision. It is the company that finds you before VA does, charges you thousands of dollars to do paperwork that costs zero, and then chases you for more after you get an increase. VA calls these operators claims predators. The Federal Trade Commission, by VA's own citation, says veterans reported $292 million in fraud losses in 2022 alone. That is not a paperwork problem. That is a cash flow problem with a friendly voice on the phone.

If you are filing an initial claim, a supplemental, or a higher-level review right now, treat this post as a pre-mission brief. Read it before you sign anything, click anything, or hand over your DS Logon to a stranger who keeps calling you "brother."

Why claims predators are a money problem, not just a paperwork problem

Most veterans I talk to think of claims predators as a paperwork inconvenience. Sloppy intake, weird forms, maybe a fee they did not expect. That framing is too soft. The damage is financial, and it lands in three places at once.

It hits your retroactive pay, because the company is positioned to take a slice the day VA cuts the check. It hits your monthly cash flow, because some operators bill on increase, meaning every time your rating goes up they show up with an invoice. And it hits the buffer you needed to ride out the months between filing and decision, because money you should have been parking went to a "consultation" that an accredited VSO would have done for free.

The Military.com report from April 14, 2026 is the most concrete example I have seen recently. A federal class-action lawsuit filed April 10, 2026 alleges that Trajector and Trajector Medical charged veterans somewhere between $4,500 and more than $20,000 for VA claims-related help. The complaint alleges veterans were not told that comparable assistance is available at no cost through accredited groups like the American Legion, VFW, or DAV, and that some veterans got hit with aggressive billing and collection pressure after their benefits went up. Important caveat: those are allegations in a lawsuit, not settled facts, and the company disputed them, saying its fees were for independent medical evidence rather than for filing claims. Either way, the price tag in the complaint tells you the size of the cash exposure veterans are walking into without realizing it.

Lose $10,000 to a predator in your forties and you did not just lose $10,000. You lost the emergency fund that would have kept you off a payday loan the next time the alternator died.

What VA actually says claims predators do

VA has been pretty direct about this on its own initiatives page and in its news posts. I am quoting their framing, not making up my own.

VA says claims predators are bad actors who unlawfully charge veterans a fee to help process VA claims. VA says it is unlawful for anyone to charge a fee for preparing an initial claim. VA says these operators often promise expedited processing or higher disability ratings in exchange for high fees, and that scammers target veterans specifically because of access to benefits and resources.

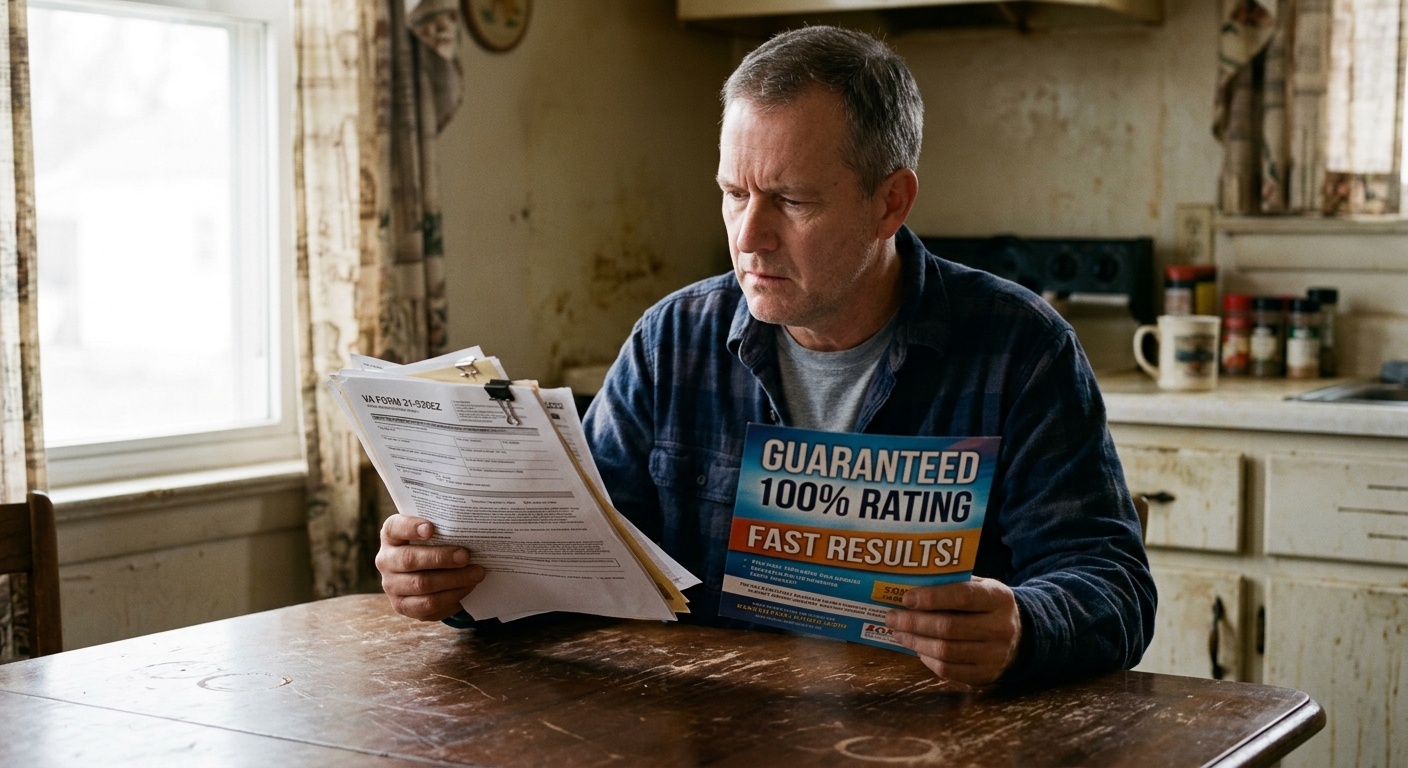

Two lines from VA's own news post are worth taping to the inside of your folder. Only VA can determine your disability rating, so any "guaranteed 100%" language is a red flag by definition. And only VA-accredited attorneys, claims agents, and VSO representatives are authorized to help with a benefits claim.

If a person or company does not fit one of those three categories, VA's position is they should not be charging you to file. That is not my opinion. That is the program speaking.

The red flags, in plain language

You do not need a law degree to spot most of these. You need a slow pulse and a willingness to walk away from a pitch that feels rehearsed.

Upfront fees on an initial claim. If they want money before VA has even decided your initial claim, you are in the wrong room. VA is explicit that charging a fee to prepare an initial claim is unlawful. There is no "consulting" workaround that fixes that.

Guaranteed ratings. Anyone who tells you they can promise a specific percentage, especially before they have read your file, is selling a feeling, not a service. VA assigns ratings based on evidence and the rating schedule. Nobody on the outside has the authority to lock that number.

Pressure tactics. The "this offer expires Friday" energy, the urgency that you sign tonight, the cold-call vibe where they will not let you off the phone. VA's fraud prevention guidance specifically lists pressure to act immediately as a sign of a scam. Real representatives are fine with you taking a week to think about it. Predators are not.

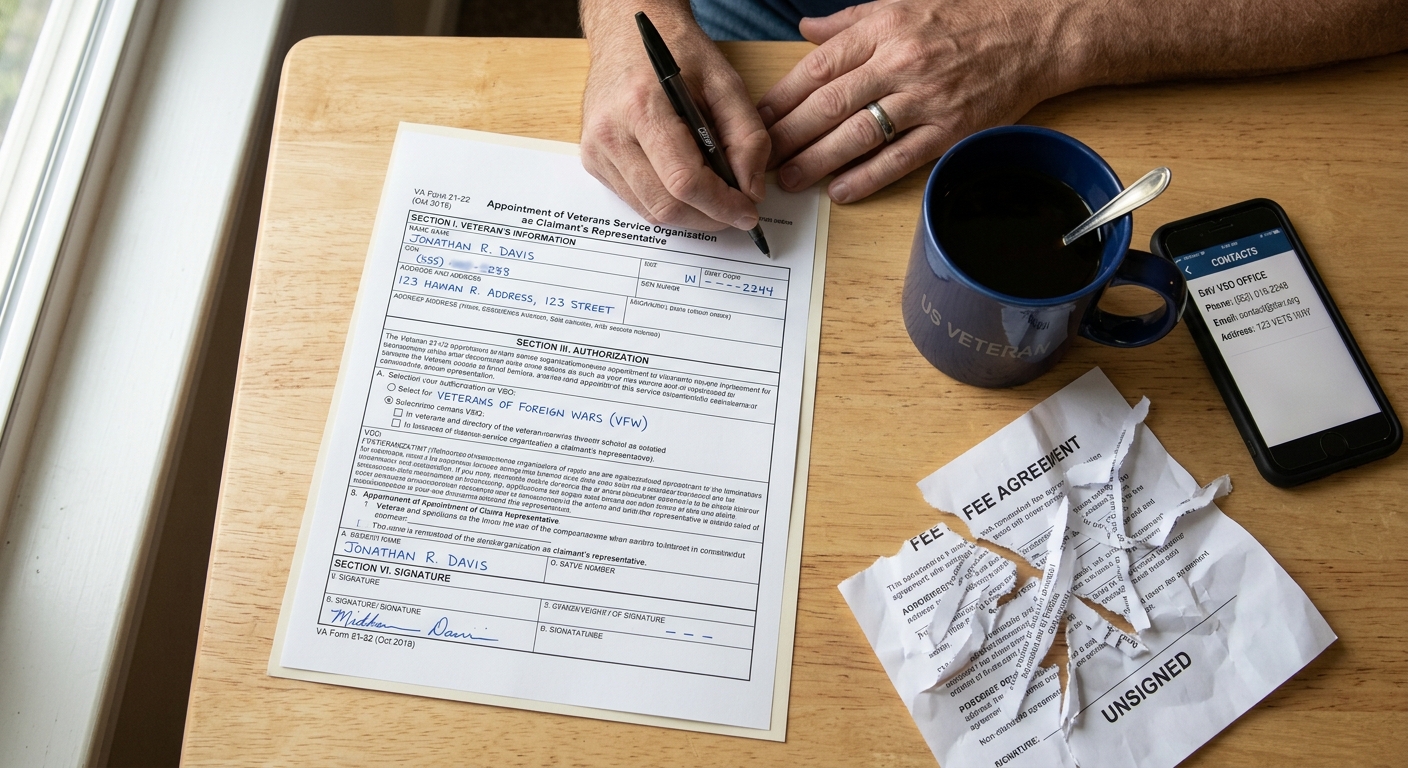

Blank or partial forms. If somebody hands you a form to sign with the fee section empty, the representation section blank, or a "we will fill in the rest later" pitch attached, stop. VA flat out says do not sign a blank form for someone else to complete later. The same goes for a fee agreement that the other side will not put in writing alongside a real VA representation form like VA Form 21-22 or 21-22a. If they will not sign the representation form, they are not your representative.

Weird payment requests. Gift cards, prepaid debit cards, cash apps, wire transfers to a personal account, crypto. VA's own guidance flags hard-to-trace payments like gift cards or electronic banking apps as a fraud signal. There is no legitimate VA-related reason to pay anyone in Apple gift cards. Ever.

Refusal to be paid through VA's direct-payment process. Here is the one a lot of veterans miss. For supplemental claims, higher-level reviews, and Board appeals, VA says you never have to make fee payments yourself if a direct-payment fee agreement is used through VA. The fee comes out of past-due benefits and goes to the representative through the VA's process. VA's own line is that if someone is unwilling to be paid that way, you should question why. That is a polite way of saying it is a red flag.

Pretending to be from a familiar organization. VA lists this one too. Spoofed names that sound like government agencies, fake "VA Benefits Department" callers, lookalike domains. Real VA-accredited reps will tell you exactly which organization they work for and let you verify them. Predators do not.

What free, legitimate help actually looks like

This is the part that the predator pitch is designed to keep you from learning.

VA accredits three categories of people to help with claims. Veterans Service Organization representatives, who work for groups like DAV, VFW, and the American Legion. Accredited claims agents, who are individuals who have passed VA requirements. And accredited attorneys, who are licensed lawyers registered with VA's Office of General Counsel. VA's position is straightforward: only those three categories should be helping you file.

VSO reps cost zero. They are not a discount. They are not a bargain. They are the actual no-cost option that the predator industry exists to keep you from finding. They will help you build the file, gather evidence, and file the right form, and the only paperwork they will hand you is a real VA Form 21-22.

Accredited attorneys and agents can charge fees, but only in specific situations after an initial denial, and the standard route goes through VA's direct-payment process so the fee is documented and capped. That is a different category from the upfront-fee, percentage-on-back-pay model that predators run.

VA also publishes its accreditation database. If a person or organization claims they can represent you, you can verify them through the VA Office of General Counsel Accreditation Search. If they are not in there, they are not accredited. If they hesitate when you say you want to verify them, that is your answer.

For background, the Trajector lawsuit referenced in the Military.com article alleges VA's Office of General Counsel sent the company cease-and-desist letters dating back to June 29, 2017 and again in January 2022, raising concerns about accreditation and fee practices. Again, those are allegations in a public complaint, not a court ruling. But the existence of cease-and-desist letters as part of the public record is a fair signal that this is not a brand-new debate inside VA.

What to do if you already shared information or signed something

If you are reading this and quietly realizing you might already be in the middle of one of these arrangements, do not panic and do not freeze. VA's own fraud guidance is clear and very actionable.

Stop contact with the company. You do not owe them another phone call, another scanned document, or another "quick question." Save the messages, the emails, the texts, and any contracts or fee agreements you signed. That paper trail matters later if you report.

Contact your bank or card issuer fast if you sent money or shared payment info. Stopping a charge in flight is much easier than reversing one that has settled. If you handed over banking info, ask the bank specifically about fraud protections and account monitoring.

Monitor your credit. VA recommends keeping an eye on it after any disclosure of personal information, and considering a credit freeze if your information was shared. A freeze is free, reversible, and stops new credit from being opened in your name without your authorization.

Report it. VA points veterans to VSAFE.gov and the 1-833-38V-SAFE phone number for fraud reporting. That puts your case into the system where it can actually be tracked.

One more piece, in plain English. If you signed a fee agreement and you think it might not be enforceable, do not just guess. Bring it to an accredited VSO or accredited attorney for a real read. They will tell you whether the document is something to push back on.

Simple cash-protection moves while your claim is in motion

The window between filing and decision is the window predators love most, because that is when you are anxious about money and most likely to say yes to a pitch. You can shrink that vulnerability without doing anything fancy.

Build a small cash floor before you file, if you can. Even one month of essential expenses parked in a separate savings account changes the math when somebody calls promising a faster decision for a fee. Money in the bank lets you say no slowly. Empty checking forces a quick yes.

Separate your benefits banking. The Veterans Benefits Banking Program, which VA highlights on its benefits administration page, exists specifically to give veterans access to banking that works well with VA deposits and includes fraud protection features. The bigger value is structural. If your VA deposit lands in an account that is not the same one your debit card runs through every day, it is harder for one bad week of spending to swallow it.

Pre-decide who you will and will not work with on your claim. Pick your VSO before you need them. Save the contact info. That way, when somebody cold-calls you with a "limited time" offer, you already have a real first call to make instead. The predator pitch only works on undecided veterans.

Treat back pay like a buffer, not a windfall. The day a retroactive deposit hits is not the day to upgrade a vehicle or pre-pay for services from a company that helped you get there. Let the deposit sit for at least a month while you confirm the rating, the math, and any fee paperwork that may be in flight against it.

Bottom line

Claims predators are not a small slice of the experience. They are a financial threat that arrives wearing the costume of a helper. VA's own position is clear. Charging a fee for an initial claim is unlawful. Only accredited reps should be helping you. Pressure, guarantees, blank forms, weird payment methods, and refusal to use VA's direct-payment process are red flags by VA's own definition. Comparable help is free through VSOs.

Your job before filing is simple. Verify accreditation, choose a VSO, refuse upfront fees on initial claims, never sign blank paperwork, and protect the back-pay deposit when it lands. If you already signed something or shared information, stop contact, save the records, contact your bank, monitor your credit, and report through VSAFE.gov or 1-833-38V-SAFE.

If you want a one-page benefits protection checklist that walks through these red flags, the accreditation verification steps, and the cash-protection moves to run while a claim is in motion, Command.ai has one ready to download. Print it, fold it into your claim folder, and use it the next time a stranger calls promising a guaranteed rating.

Share this article

Help others discover this content

Related Articles

How Veterans Can Build a Cash Buffer Before a Tech Career Pivot

A tech pivot without cash on hand turns every small setback into a debt event. Here is how to size a real buffer, decide between saving and paying off debt when income is unstable, and use VA benefits and the GI Bill as baseline income without building a budget on temporary money.

Veterans May Be Owed 12 Extra Months of GI Bill Benefits Thanks to Two Court Rulings

Two court decisions — Rudisill at the Supreme Court in 2024, Perkins at the Court of Appeals for Veterans Claims in 2025 — forced the VA to reopen the math on GI Bill entitlement. The VA says the combined effect could reach roughly 2 million veterans, many of them owed up to 12 additional months. Here is what each ruling actually changed, who it covers, and the short list of things to do this week.

The New Military Financial Literacy Act: What Veterans Need to Know in 2026

A bipartisan bill just passed that could change how veterans learn about money. Most have not heard of it yet. Here is what it actually does, why it matters, and what you can do right now.