How Veterans Can Build a Cash Buffer Before a Tech Career Pivot

I keep meeting veterans who are six weeks from quitting their job to learn to code. They have a Coursera tab open, a half-finished resume, a vague plan to "use the GI Bill," and about $1,800 in checking. That is not a plan. That is a runway shorter than most Reserve drill weekends.

The pivot is real. The job market for veterans in tech-adjacent and government-adjacent roles is genuinely opening up. But every week I see somebody burn through their last cushion in month two of a six-month transition, then take a payday loan or a high-interest credit advance to keep the lights on, then quietly drift back to a warehouse job because the math fell apart. The pivot was correct. The cash position was wrong.

This post is the cash conversation I wish more recruiters and bootcamp marketers had with veterans before they cashed out a TSP or signed up for a $15,000 program. Save first. Then pivot.

Why a tech pivot without cash is risky, even when the long-term upside is real

The career math on a tech pivot can look great on paper. A junior software role, a federal IT contract, a VA-adjacent product job — any of those can clear what a lot of veterans are making in their first post-service civilian gig. The problem is not the destination. The problem is the runway between here and there.

A pivot without cash does three predictable things. It forces you to take the first offer instead of the right offer. It pushes you toward high-interest debt the moment something normal happens, like a brake job or an ER copay. And it puts pressure on your spouse, your parents, or whoever is quietly subsidizing the gap, which has its own slow cost that does not show up on a balance sheet.

The Fortune piece from April 23, 2026 on whether to save or pay down debt put it cleanly: when income is unstable, cash on hand matters more than a lower debt balance. That is the whole game in a transition. You are voluntarily making your own income unstable for a stretch. The way you survive that stretch is liquid money, not a slightly better debt-to-income ratio.

What a cash buffer actually covers during a transition

Most veterans I talk to underestimate the buffer because they only count rent. A real transition buffer covers the boring monthly stuff plus the friction costs of looking for work. Walk through it line by line:

- Rent or mortgage. Including renter's insurance and any HOA. Not the discounted "I cut grocery spending for a month" version. The honest one.

- Utilities and internet. Internet is non-negotiable in a tech pivot. Treat it like rent.

- Food. Realistic groceries plus a small allowance for the actual amount you eat out. Pretending the eating-out line is zero is how budgets quietly fail in week three.

- Transportation. Gas, insurance, registration, and a buffer for the $400 repair that always arrives at the worst moment.

- Health. If you are not 100% P&T, anything VA does not cover plus copays, prescriptions, and dental.

- Debt minimums. Not the payoff plan. Minimums. Anything above minimums is a different conversation that comes later.

- Interview and job search costs. The line nobody puts in their budget. A clean shirt, a haircut, a printed resume, a parking garage downtown, gas to a second-round on-site, a $40 LinkedIn Premium month, the occasional cert exam fee. Two hundred dollars a month is a reasonable starting estimate. It is rarely zero.

Add those up honestly for one month. That is your essential burn rate. The Fortune piece references the standard 3 to 6 months of essential expenses as the emergency fund target. For a transition, I would push the floor up. Three months is what you keep for an unexpected layoff while you still have income coming in. For a deliberate, planned pivot where you are choosing to slow your income, six months is the realistic floor and nine is better. You are not preparing for a surprise. You are preparing for a known gap.

Save first or pay down debt first when income is unstable

This is the question I get most. The honest answer is that it depends on the interest rate and how fragile your income is, and you can usually do a small version of both.

The Fortune framing is the right starting point. High-interest credit card debt, the 22 to 29% APR stuff, is a five-alarm fire and usually beats a savings account on pure math. But cash on hand is what keeps you from adding a sixth alarm next month when the alternator goes. So the sequence most veterans should run, in plain language:

- Build a small cash floor first. Call it one month of essential expenses. That single buffer prevents the next surprise from going on a credit card and undoing whatever debt progress you make.

- Once that floor exists, attack the highest-rate debt with everything above the floor. Card balances above 20% APR get hit first. The math is brutal in their favor; do not negotiate with them.

- Lower-rate debt, like a 6% car loan or a 4% federal student loan or a fixed-rate mortgage, is not the priority during a transition. Pay the minimum. Direct the extra cash toward the buffer.

- Once the high-rate debt is gone, finish building the full transition buffer. Three months minimum if you still have income, six or more if you are about to walk away from a paycheck on purpose.

The exception is anyone with truly catastrophic interest like payday loans or title loans. Get out of those before anything else. You cannot save your way past a 300% APR.

Using VA benefits and school benefits as baseline income without building a fake budget

This is the part where a lot of veterans fool themselves. VA disability compensation is real income. Post-9/11 GI Bill housing allowance is real income. VR&E subsistence is real income. They all hit your account on a schedule. So why not budget against them?

Because some of them are temporary, some of them are conditional, and some of them disappear the moment a circumstance changes. Building a fixed monthly budget on a temporary income stream is how veterans end up upside down when the stream ends.

A useful way to sort it:

- VA disability compensation: baseline. As long as your rating holds, this is recurring monthly income you can plan around. Build essential expenses around the portion you actually receive after any allotments.

- Post-9/11 GI Bill housing allowance (MHA): conditional. It only pays while you are enrolled at the right rate of pursuit, it varies by ZIP code and term, and it stops the moment you drop below half-time or finish out a term. Plan it as cover for school-period rent, not as a permanent paycheck.

- VR&E subsistence allowance: program-dependent. It exists while you are in an approved plan and ends with the plan. Useful as a transition stipend, dangerous as a long-term assumption.

- Severance, unused leave payouts, or one-time deposits: buffer, not recurring income. The temptation is to mentally divide a $9,000 payout across nine months at $1,000 a month and live like that is your salary. It is not. It is the buffer itself.

The cleanest discipline is to build two budgets in the same spreadsheet. The first is your survival budget on baseline income only — what you can sustain on the recurring stuff. The second is your accelerated budget that uses the temporary stuff to pay down debt faster or to invest in a credential. Keep them visually separate. When the temporary stream ends, you fall back to the survival budget without redesigning your life.

What federal tech transition signals matter right now

There are real signals in the room that should make veterans bullish about a tech pivot, but they should be read as opportunity, not as permission to burn cash.

The VA's FY 2027 budget request, posted April 20, 2026, asks for $488.2 billion, a 7.7% increase above the FY 2026 enacted level. That includes $337.6 billion in mandatory funding, up $22.6 billion or 7.2% above 2026, covering Compensation and Pensions, Readjustment Benefits, Housing and Insurance, and continued Toxic Exposures Fund support. The request signals continued investment in the benefit programs a lot of veterans depend on.

Important caveat: a budget request is not money. It moves through OMB and Congress and gets shaped along the way. You should treat it as directional information about where the system is pointing, not as a check you can budget against personally before the appropriations are final.

On the tech side, the GSA announcement from April 23, 2026 about the 2026 Presidential Innovation Fellows class is worth reading carefully. Seventeen technology experts are being embedded at ten federal agencies, including the Department of Veterans Affairs, with GSA specifically saying the fellows will help establish an AI-ready VA workforce and execute AI and automation initiatives that improve veteran care delivery.

That is a meaningful signal. It tells you tech talent is still strategically valuable inside government and government-adjacent spaces, and that the VA in particular is investing in AI capability. For a veteran who can credibly bridge military experience and software, the demand is there. What it does not tell you is that there is a job waiting for you the day you finish your bootcamp. Treat the signal as a green light to invest in skills. Do not treat it as a green light to skip the cash buffer.

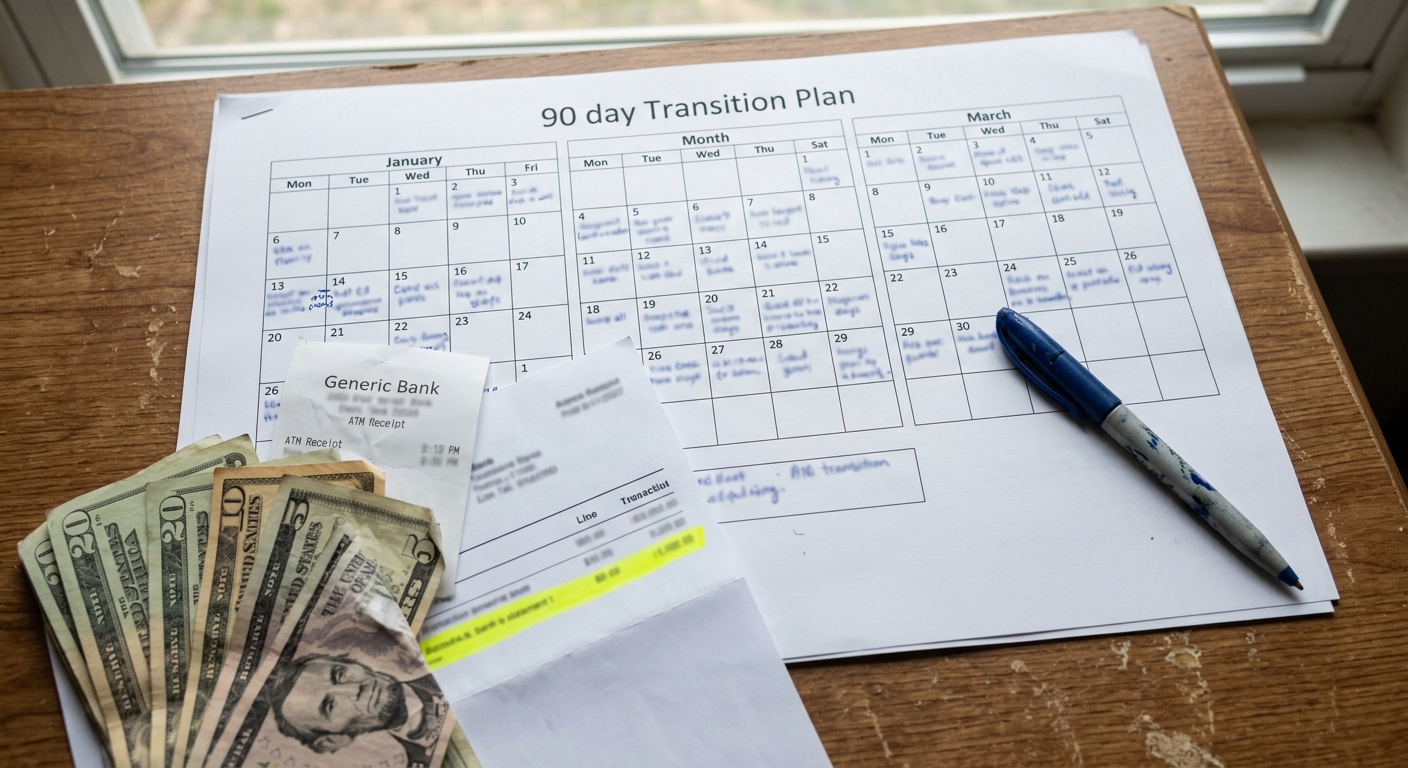

A simple 90-day buffer plan before starting the pivot

If you are six months out from a planned pivot, whether that means leaving a job, starting a program, or going full-time on a job hunt, here is a 90-day plan that gets you to a defendable starting position. None of this is fancy. It is what works.

Days 1 through 30: Get honest about the number. Pull three months of bank and card statements. Add up actual spending in the categories above. Subtract one-time anomalies. Multiply your real essential burn rate by six. That is your transition target. Write it down somewhere you will see it. If it scares you, good. That number is the size of the gap your previous "I'll figure it out" plan was hiding.

Days 31 through 60: Cut, automate, and start the floor. Find $200 to $500 a month in cuts. Subscriptions, the second streaming service, eating out, the gym you did not go to in February. Set up an automatic transfer into a separate high-yield savings account on the day after each payday. Build the first month of buffer before anything else. If you have credit card debt above 20% APR, send anything above that first month's buffer at the highest-rate card.

Days 61 through 90: Pre-stage the pivot. While the buffer is building, spend evenings de-risking the pivot itself. Confirm your GI Bill or VR&E status with the VA in writing. Get a Statement of Benefits. If you are planning to use the Post-9/11 housing allowance, look up the actual MHA for your ZIP and rate of pursuit so you know what you will receive, not what you assume. Update your resume, get one informational conversation in your target field, and apply to two or three positions to test the market. The pivot day stops being a leap when you have already taken three small steps off the cliff.

At the end of 90 days, you will have a real number, a real cash floor, a clearer view of which benefits will actually hit your account during the gap, and some early signal from the job market. None of that requires you to quit your job or enroll in a program. All of it makes the pivot survivable when you do.

Bottom line

A tech career pivot is a financial event before it is a career event. Veterans who survive the gap are not the ones with the best resumes. They are the ones who built a real cash buffer first, sized it to honest expenses, used VA and school benefits as baseline income without overcommitting to temporary streams, and treated the federal tech signals as a tailwind, not a guarantee. Save first. Pivot second. Stack the deck before you draw the cards.

If you want a structured way to size your own buffer and lay out a 90-day plan on one page, Command.ai's cash-buffer calculator and transition budget template walk you through the line items above and split your inputs into baseline VA income vs temporary streams, so the budget you build still works the day the temporary money stops.

Share this article

Help others discover this content

Related Articles

Veterans May Be Owed 12 Extra Months of GI Bill Benefits Thanks to Two Court Rulings

Two court decisions — Rudisill at the Supreme Court in 2024, Perkins at the Court of Appeals for Veterans Claims in 2025 — forced the VA to reopen the math on GI Bill entitlement. The VA says the combined effect could reach roughly 2 million veterans, many of them owed up to 12 additional months. Here is what each ruling actually changed, who it covers, and the short list of things to do this week.

The New Military Financial Literacy Act: What Veterans Need to Know in 2026

A bipartisan bill just passed that could change how veterans learn about money. Most have not heard of it yet. Here is what it actually does, why it matters, and what you can do right now.

How Veterans Can Build an Emergency Fund With VA Benefits Without Killing Cash Flow

Living on VA disability, GI Bill stipends, or mixed benefit income does not mean you cannot save. Here is a practical ladder from your first $500 to three months of expenses, built around the money you actually receive.