VA Overpayment Notices in 2026: How Veterans Can Fight Debt Without Wrecking Their Budget

If a letter from the VA Debt Management Center just landed in your mailbox, take a breath before you do anything else. That envelope is alarming on purpose. It is not, however, a verdict. It is a notice with a clock attached, and the worst thing you can do is shove it in a drawer and hope the next benefit deposit shows up the way it always has.

I have watched too many veterans treat an overpayment letter like a parking ticket. Open it next week. Maybe call sometime. By the time they actually engage with it, VA has already started offsetting their monthly benefits, the debt has been kicked to Treasury, and a tax refund they were counting on for spring is gone. That is the version of this story I want to help you avoid.

What a VA overpayment notice actually means

VA is telling you, in writing, that at some point it paid you more than its records say you were entitled to. That is it. Per VA's debt management page, the most common causes are unreported life changes, life changes reported too late to catch the next payment cycle, and VA errors like a double payment. Dependency changes, school enrollment changes, and rating adjustments show up over and over in the real-world cases.

So before you panic about a number, ask the boring question first. Is this real? VA pays a lot of benefits. VA also makes mistakes. The letter is the start of a conversation, not the end of one.

Your first move is to find out what VA actually has on the books. You can review balances for disability compensation, pension, education overpayments, and health care copays online at va.gov/manage-va-debt. The Debt Management Center phone line is 800-827-0648, Monday through Friday, 7:30 a.m. to 7:00 p.m. Eastern. VA itself warns that if you are paying off a full balance or you are still receiving monthly benefits, you should call first to confirm the exact number so you do not overpay. That advice is sitting right there on the official page. Take it.

There is also an active scam alert tied to VA overpayments. People are getting calls demanding immediate payment, gift cards, that whole playbook. The Debt Management Center will not work that way. If anyone pressures you to pay outside of VA's normal channels, hang up and call VA directly.

The 2026 deadlines that matter now

This is the part of the post I want you to dog-ear. Deadlines on a VA debt letter are not suggestions. They are the difference between a manageable problem and an expensive one.

30 days. If you dispute the overpayment within 30 days of the first debt letter, VA says collection actions can be paused while the dispute is considered. That is the window where you have the most leverage and the least pressure on your monthly check.

30 or 90 days, depending on the debt. If you are requesting a waiver and want to stop collection while VA decides, the cutoff is 30 days from the first debt letter for education overpayments, and 90 days for disability compensation or pension overpayments. Different programs, different stopwatches. Read your letter for which one applies.

120 days. After that, delinquent debt gets referred to the U.S. Treasury. That is when the math turns ugly, and we will get to that in a minute.

1 year. This is the deadline most veterans do not know about. VA can only consider waiver requests made within one year of the date you received your first debt letter. That window is spelled out in VA's waiver guidance and in Volume XII Chapter 11 of VA's financial policy, approved October 28, 2025, which notes VA is updating 38 CFR 1.963 to align with the one-year rule. If you are reading a letter from last summer and you have been ignoring it, the waiver door may be closing on you faster than you think.

The three response paths

There are basically three doors you can walk through after you get an overpayment notice. Pick one based on the actual facts of your situation, not based on which one feels least scary.

Door 1: Dispute the debt

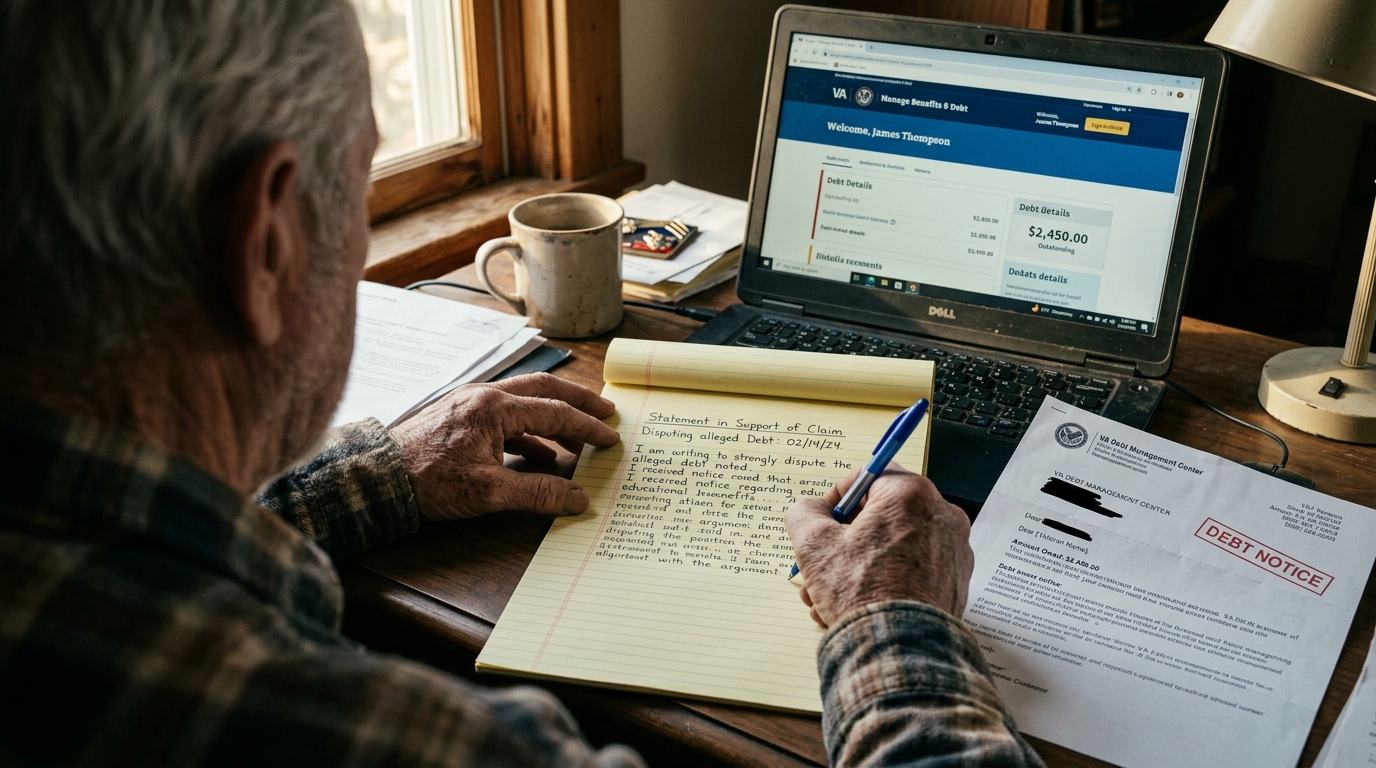

Use this one if you do not think you owe the money. Maybe VA is missing a status change you already reported. Maybe the dates are wrong. Maybe it is a flat-out error. You can dispute the debt with a written statement, online through Ask VA, or by mail to the Debt Management Center, PO Box 11930, St. Paul, MN 55111.

Two things to know. First, this is the move that buys you the 30-day collection pause, so move fast. Second, write the dispute like you are explaining it to a stranger. Dates, supporting documents, plain language, no theatrics. If you submitted a dependency change on a specific date, name the date and attach proof. The point is to make it easy for whoever opens your file to agree with you.

Door 2: Set up a repayment plan

Use this one if you owe the money, or you probably owe the money, and you can pay it back in less than five years. VA will set up a repayment plan online, by phone, or by mail. If you need five years or more to pay it off, VA requires VA Form 5655, the Financial Status Report, so they can see the math.

The honest read on this door is that for a lot of veterans, a repayment plan is the right answer even if a waiver is theoretically possible. The reason is speed and certainty. A plan you set up this month protects your monthly benefit from a sudden full offset and keeps the debt out of Treasury. A waiver fight you might win in six months does not put rent on the table this month.

Door 3: Request a waiver or compromise

Use this one if you owe the money on paper but paying it back would create a real financial hardship, or if there is a fairness argument that VA itself should consider. A waiver means VA forgives part or all of the debt. A compromise is an offer to settle for less than the full amount.

Both require VA Form 5655. A waiver also requires a personal statement explaining why you should not have to repay. That statement is where your real story goes. Job loss, medical bills, the dependency change you reported on time that nobody processed, the income drop that makes the original calculation unfair now. Stick to the facts. Document what you can.

And remember the one-year waiver clock. If you miss it, this door closes for that debt.

What happens after 120 days, and why delay gets expensive

This is the part veterans underestimate. If you do nothing, VA's own guidance says it may offset part or all of your monthly benefits, report the debt to credit bureaus, and add interest for certain debt types. That alone is rough. But after 120 days of delinquency, VA refers the debt to the U.S. Treasury.

Once Treasury has it, the consequences expand. Treasury can add its own fees and interest. It can offset your tax refunds. It can offset Social Security benefits. It can hand the debt off to a private collection agency. That is where a $1,400 overpayment turns into a $1,900 problem, a missing tax refund in April, and a stranger calling your phone. The actual dollar amount may not change much in VA's records, but the friction and the side damage do.

None of that has to happen. The window between the first letter and Treasury referral is the entire game. If you call inside 30 days, you have access to dispute pauses, waiver collection holds, and repayment plans that VA actually wants to set up. If you call after Treasury referral, you are negotiating with different people under worse terms.

How to protect rent, bills, and monthly cash flow

Now the financial-literacy part. Whatever path you choose with VA, you need to protect the rest of your life while it plays out.

Assume your next deposit might be smaller. Until you have a dispute pause, a waiver collection hold, or a repayment plan in writing, do not budget the next benefit deposit at its full amount. Plan as if VA could offset some or all of it. That is not paranoia. That is what VA tells you it can do if you do nothing. Build the worst case into this month's numbers and adjust upward only when you have something in writing.

List your non-negotiables first. Rent or mortgage. Utilities. Insurance. Groceries. The minimum payments that keep your credit from cratering. Add them up. That is the line your cash flow has to clear, full stop. Everything else is negotiable until this is settled.

Call your landlord or lender before you miss anything. If the worst case has you short on rent for one month, the conversation you want is the one that happens before the due date. A landlord who hears from you on the 25th about a possible partial payment on the 1st is a different person than a landlord who hears from you on the 10th after the check bounced. Same for car notes, utilities, and credit cards. Most of them have hardship programs they will not volunteer until you ask.

Park anything optional. Subscriptions, the second streaming service, the gym you have not used in three months, the auto-renew you forgot about. Pause them this week. You can turn them back on when the dust settles. The point is to free up cash you do not have to ask anyone's permission to free up.

Know your real safety net. Military OneSource, branch relief societies, USA Cares, Operation Homefront, VFW Unmet Needs, American Legion Temporary Financial Assistance. These are not tied to your VA debt status. They exist for exactly this kind of one-time cash crunch. Some veterans treat them as a last resort and end up missing rent first. They are not a last resort. They are a tool.

Document every contact with VA. Dates, names if you can get them, what was said, what was promised. Keep the originals of every letter and the confirmation of every submission. If something later goes sideways with a dispute or a waiver, the file you built is your best argument.

The honest read

A VA overpayment notice is not a moral verdict on you. Plenty of these letters come from VA's own processing delays. Plenty more come from life changes that were reported on time but never made it into the right field in the right system. Some of them are real debts, and even then the rules give you real options to dispute, waive, compromise, or pay over time.

What the system does not give you is forgiveness for ignoring it. Thirty days. Ninety days. One year. One hundred and twenty days to Treasury. Every one of those deadlines is in writing on official VA pages. Once you know them, the playbook is straightforward. Open the letter. Verify the debt. Pick a door. Protect the rest of your budget while you walk through it.

That is how veterans come out of this with their housing intact, their credit intact, and their benefits intact. Not by being lucky. By being on the clock.

Download the VA debt response checklist

I built a one-page checklist that walks through the moves above in order. Verifying the balance with the Debt Management Center, choosing among dispute, repayment, waiver, or compromise, the deadline calendar with the 30-day, 90-day, 120-day, and one-year marks, the cash-flow protection steps for rent and bills, the documentation list for VA Form 5655 and the waiver personal statement, and the relief-society contact list for short-term gaps. It is built around VA's own debt management, options-for-help, waiver, and policy pages so the rules stay accurate to what is in print as of early 2026.

Download the VA debt response checklist and run it the same day your letter arrives, not the week after.

Sources: VA, "VA debt management," va.gov/resources/va-debt-management/, updated January 30, 2026; VA, "Options to request help with VA debt," va.gov/resources/options-to-request-help-with-va-debt/, updated February 9, 2026; VA, "Waivers for VA benefit debt," va.gov/resources/waivers-for-va-benefit-debt/; VA, "Manage your VA debt," va.gov/manage-va-debt/, updated February 9, 2026; Department of Veterans Affairs, Financial Policy Volume XII Chapter 11, "Waiver Requests and Processing (COWC)," approved October 28, 2025.

Share this article

Help others discover this content

Related Articles

VA Disability Back Pay in 2026: How Veterans Should Use a Lump Sum Without Wrecking Their Budget

A back-pay deposit is months of compensation arriving in one shot. The math behind that number is the effective date, and the smartest move in the first 72 hours is verifying it before you spend a dollar.

VET TEC 2.0 vs. VR&E in 2026: Which Tech Training Path Makes More Sense for Veterans?

VET TEC 2.0 and VR&E both fund tech training, but they were built for very different veterans. Here is how to pick the right lane in 2026 without burning the wrong benefit or wrecking your cash flow.

VR&E vs. the GI Bill in 2026: Which Benefit Should Veterans Use First?

VR&E and the Post-9/11 GI Bill solve different problems. The wrong sequence costs veterans entitlement, housing money, or both. Here is the plain-English read on which one to use first in 2026, with the official VA rules and a few honest mistakes to avoid.