VA Disability Back Pay in 2026: How Veterans Should Use a Lump Sum Without Wrecking Their Budget

If the deposit hit and your bank balance suddenly looks like a typo, you are not alone. VA disability back pay has a way of arriving without much warning, and the number is almost always bigger than veterans expect. I have watched guys go from rationing the gas tank to staring at a five-figure deposit in the same week. That swing is the trap. The money is real, the relief is real, and the first thing most people do is the wrong thing.

This post is about how to handle that lump sum without blowing the runway it just gave you. Not a lecture. A plan. The kind of plan I wish someone had walked me and every veteran I have helped through before the deposit ever landed.

What back pay actually is, in plain English

VA disability compensation is a monthly tax-free payment for a service-connected condition. That is straight from VA's own disability page. When a claim takes months or years to work through the system, VA owes you the months you were entitled to but did not receive. That gap, paid in a single deposit, is what veterans call back pay.

The size of the check is not random. It is the monthly compensation rate, times the number of months between your effective date and the day VA actually started paying. Two veterans with the same rating can get wildly different back-pay numbers because their effective dates landed in different places. That is the part of the system most people do not understand until the deposit shows up.

So before you touch the money, make sure you know what the deposit is supposed to be. The award letter spells out the effective date, the rating, and the monthly amount. The math has to line up. If the deposit is off by a month or two of compensation, that is real money you are entitled to. It is also money that gets harder to claw back the longer you wait.

Why the effective date controls everything

The effective date is the day VA says you became eligible for the benefit. Every dollar of back pay traces back to it. VA's own page on effective dates lays out four common scenarios, and they are worth knowing cold because they decide whether your check is a few months or a few years of compensation.

- Direct service connection. The effective date is whichever is later: the date VA got your claim, or the date the illness or injury first arose.

- Claims filed within one year of separation. If VA got your claim within a year of leaving the service, the effective date can go back as early as the day after separation.

- Reopened claims. The effective date is the date VA got the request to reopen, or the date the condition first arose, whichever is later. Old denied claims do not automatically pull the date back to when you first filed.

- Increases in disability. If your condition got worse and VA grants a higher rating, the increase can backdate to the earliest day you can prove the condition worsened, but only if VA got the new claim request within one year from that date. Miss that window and the effective date is just the day VA got the claim.

That last one quietly costs veterans the most. If your knee got noticeably worse two years ago and you finally filed last month, the rule pulls your effective date forward to the filing date, not the day your symptoms changed. The two-year gap between when you got worse and when you filed is gone. There is no back pay for it.

This is also why the day-after-separation rule for new claims is such a big deal. A vet who files inside that first year locks in months of back pay automatically while VA works the claim. A vet who waits eighteen months loses that runway and only starts the clock when VA receives the paperwork. Same condition, same rating, very different check.

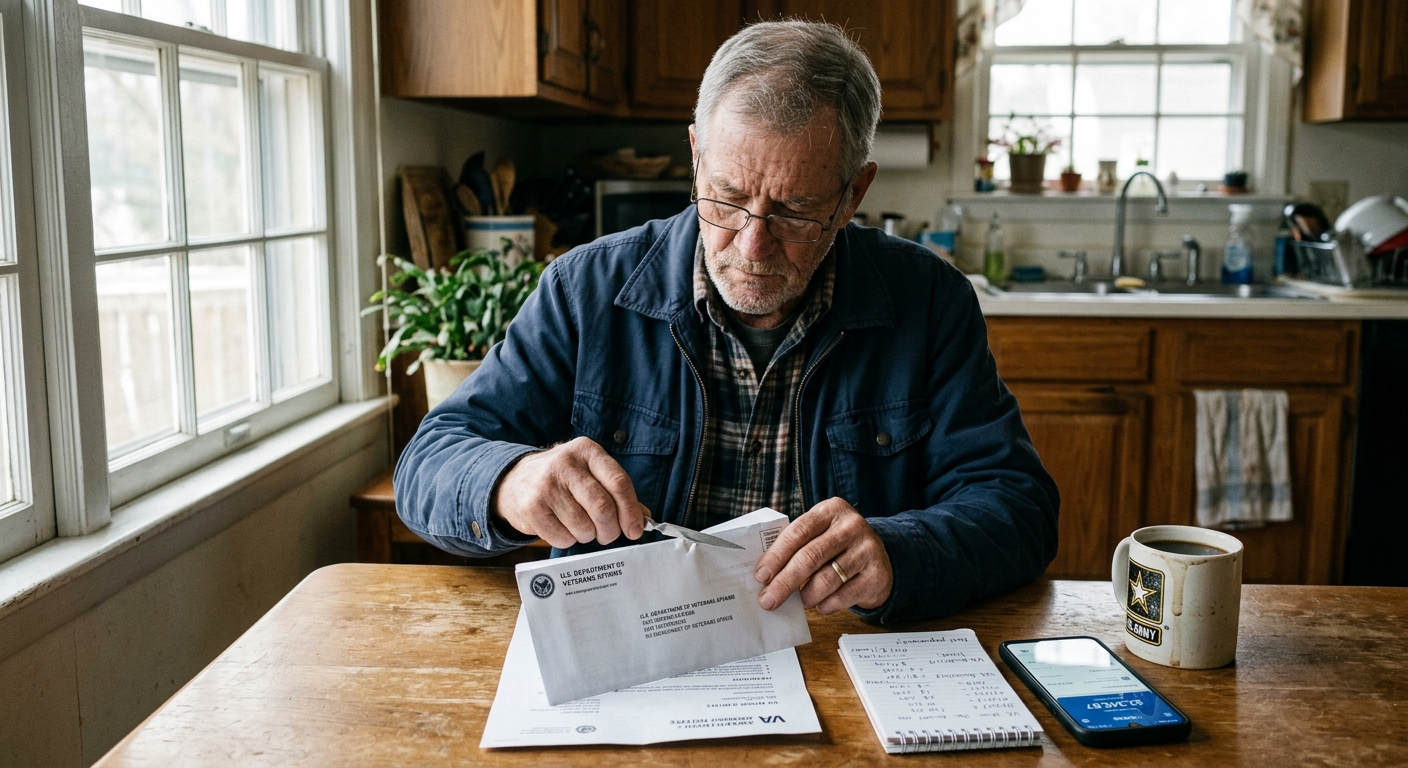

The first 72 hours after the money lands

The deposit hitting is not the finish line. It is the moment you have the most leverage to catch a mistake or confirm everything is right. Spend the first three days doing the boring verification work before you spend a dollar.

Read the award letter line by line. Not skim. Read. Look for the effective date, the rating percentage for each condition, the monthly amount, and the number of months VA is paying. If you have dependents and you are rated at 30 percent or higher, VA's payment history page confirms that you may be eligible for a higher monthly amount once they are added. Check that the letter reflects who is actually on your record.

Pull your payment history online. VA's payment history tool shows past VA payments for disability compensation, pension, and education benefits. That is your independent record. Cross-check the deposit against what the award letter says you are owed. If the numbers do not match, the gap is your starting point for a call.

Confirm direct deposit is still pointed at the right account. VA tells veterans to update direct deposit, address, and other contact information when anything changes. People move, switch banks, close old accounts. Back pay sometimes lands in the wrong place because no one updated the file. If your account changed between filing and decision, verify the routing now, not after the next monthly payment goes sideways.

Confirm dependents are on the record. If your rating is 30 percent or higher, eligible dependents can mean a higher monthly amount going forward. If you added them right before the decision, make sure they are reflected in the award. If you did not add them yet, that is the next paperwork to fix, because every month it sits is a smaller deposit than you are entitled to.

Check timing against what VA publishes. If a decision notice shows a rating of at least 10 percent, VA says the first payment should arrive within 15 days. If your award letter says one number and 15 days have come and gone with nothing in the account, something is off and the Debt Management Center or the regional office needs a call.

One more piece of context. VA announced on April 15, 2026 that average disability claim completion time dropped from 141.5 days to 80.7 days, that claims-processing accuracy is up to 94.02 percent, and that the disability backlog fell below 100,000 claims in February 2026 for the first time since 2020. That is good news for veterans still waiting. It also means the system is moving faster, which is exactly when verification errors slip through. Faster is not the same as flawless. Check the math.

A smart allocation order for the lump sum

Once you have confirmed the deposit is right, you can stop verifying and start allocating. The order matters more than the percentages. Most veterans I talk to do this in the wrong sequence and then wonder why a five-figure deposit is gone in four months.

Step one. Catch up the essentials. If rent is behind, electric is shut off, the car insurance lapsed, or the kids' medical bills went to collections while you waited, this is what the money is for first. Not a celebration dinner. Not a new TV. The boring stuff that was bleeding you while the claim sat. Pay the past-due rent. Get the utilities current. Reinstate the insurance. Pull the accounts that went to collections back to a place you can actually negotiate from.

Step two. Build an emergency buffer in cash. One full month of rent, utilities, food, transportation, and medication, sitting in a checking or savings account you can move from the same day. Then a second month. The whole point of a buffer is that the next time a deposit is late, a rating changes, or something breaks, you do not slide back into the same hole the back pay just pulled you out of. This is the single highest-leverage move you can make with a lump sum, and it is the one most veterans skip because it feels boring.

Step three. Pay down the ugly debt. Not all debt is the same. Payday loans, title loans, store-card balances at 25 percent, and anything in active collections are the ugly debt. That is what you kill next. A 0 percent car loan is not the priority. A balance-transfer card you still have a year of intro APR on is not the priority. Hit the stuff bleeding you at double-digit interest first, in full where you can.

Step four. Top off the buffer and the basics. If there is still money left, push the buffer to three months of expenses. Replace the threadbare tires. Fix the dental work you have been putting off. Buy the work boots that actually fit. None of that is glamorous. All of it pays back.

Step five. Then, and only then, talk about the wants. If you have caught up the essentials, built two to three months of buffer, killed the ugly debt, and handled the basics, the rest is yours to enjoy without it wrecking your runway. A weekend with the family. A meaningful upgrade. A small investment. Whatever it is, you earned it, and at this point spending some of it will not undo the work you just did.

One thing I keep telling veterans: this is a one-time event. Back pay is not a paycheck. You are not getting another one next month. Treat it like the rare, finite resource it is.

Common mistakes veterans make with back pay

I have seen these patterns enough times to know they are not random. They are what happens when months of financial stress release all at once.

- Treating the deposit like income. Back pay is months of compensation paid in one shot. It is not a raise. The mistake is upgrading rent, the car, or the lifestyle to a level that monthly compensation alone cannot sustain. Then the buffer is gone and the new fixed costs are still there.

- Skipping the award letter. The letter is how you know the number is right. Veterans who skip it are the ones who find out a year later that VA underpaid or that the effective date in the system is wrong and the window to fix it without a fight has closed.

- Loaning it out. Family and friends find out fast that the deposit landed. A loan to a relative who is also struggling rarely comes back, and now the buffer you needed is in someone else's checking account. If you want to help, give a small gift you can fully afford to lose. Do not lend out the runway.

- Paying off the wrong debt. Wiping out a low-interest VA-backed mortgage with back pay sounds responsible. It is usually wrong. That money would be doing more work as a cash buffer or against a payday loan at triple-digit rates. Match the payoff to the cost of the debt, not the size of the balance.

- Buying a depreciating asset on payday. A used truck on the day the deposit lands is a story I have heard more times than I can count. Wait two weeks. If you still want the truck after the rest of the plan is set, fine. Most of the time, two weeks of distance is enough to talk yourself out of the worst decision.

- Forgetting the dependent piece. A 30 percent or higher rating may qualify you to add eligible dependents for a higher monthly payment going forward. Not adding them is leaving money on the table every single month after the back pay clears.

- Ignoring the next claim window. If there is another condition you have been documenting, or a rating you think should be higher, the year-from-worsening rule on increases starts running the day you can prove the condition got worse. Sitting on the paperwork costs back pay you could have locked in.

The cleanest version of this whole plan is short. Verify the deposit. Catch up. Build the buffer. Kill the ugly debt. Then enjoy a piece of what is left. You can be aggressive about the verification, slow about the spending, and ruthless about the order. That is the version of this that protects the runway.

Download the back pay allocation worksheet

I built a worksheet for the exact sequence in this post. It walks through verifying the award letter, checking the effective date against VA's rules, pulling your payment history, confirming dependents and direct deposit, and then allocating the deposit in the order above. It is built around VA's own published rules, so it lines up with what your award letter actually says.

Download the back pay allocation worksheet and use it before you spend the first dollar.

Sources: VA, Disability compensation overview, last updated May 11, 2026 (va.gov/disability/); VA, Effective dates for disability claims, last updated May 15, 2024 (va.gov/disability/effective-date/); VA, VA payment history, last updated May 8, 2026 (va.gov/va-payment-history/); VA News, "VA announces major improvements in benefits processing and delivery," April 15, 2026 (news.va.gov/press-room/va-announces-major-improvements-in-benefits-processing-and-delivery/).

Share this article

Help others discover this content

Related Articles

VET TEC 2.0 vs. VR&E in 2026: Which Tech Training Path Makes More Sense for Veterans?

VET TEC 2.0 and VR&E both fund tech training, but they were built for very different veterans. Here is how to pick the right lane in 2026 without burning the wrong benefit or wrecking your cash flow.

VA Overpayment Notices in 2026: How Veterans Can Fight Debt Without Wrecking Their Budget

A VA debt letter is not a verdict. It is a clock. Here is what the 2026 rules actually say, the three response paths you have, and how to keep rent and bills safe while you sort it out.

VR&E vs. the GI Bill in 2026: Which Benefit Should Veterans Use First?

VR&E and the Post-9/11 GI Bill solve different problems. The wrong sequence costs veterans entitlement, housing money, or both. Here is the plain-English read on which one to use first in 2026, with the official VA rules and a few honest mistakes to avoid.